Let’s talk about why FD is a bad idea and the importance of equity and the risks associated with equity in this article.

Before getting into the main topic FD, we should be knowing about equity and inflation.

What is Equity?

As discussed in my previous article, Equity is nothing but stocks or shares of the companies you own. When you hear the word equity it means equity mutual funds or direct investment in the stock market.

What is Inflation?

Before getting to know the importance of equity, we need to know the concept of inflation. What is inflation? Let me explain with an example.

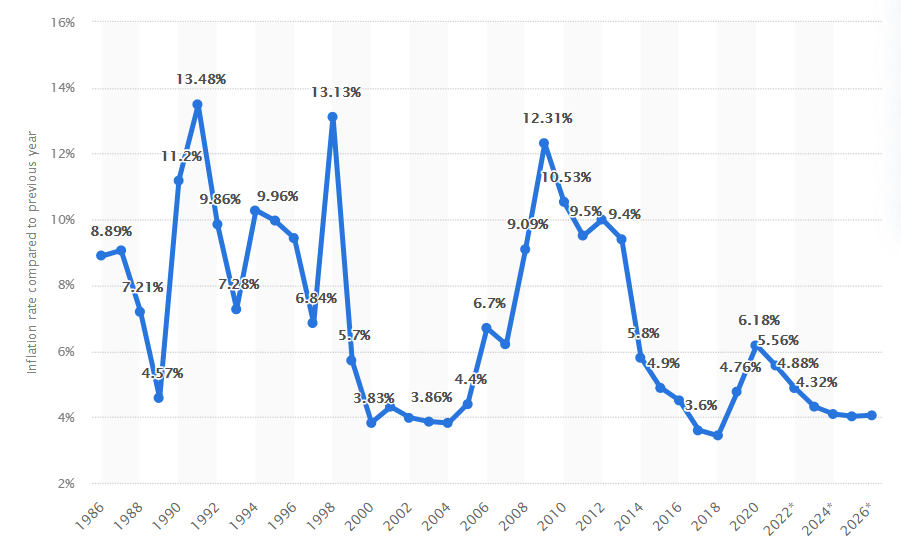

You are buying 2kg of rice for ₹100 today. After 1 year, you are buying the same 2kg of rice for ₹115. Then the inflation rate is said to be 15 percent. Usually, you won’t see such a high inflation rate and the current inflation rate is 5.56% for the year 2021 as shown in the below image. You can also notice that the inflation rate was highest during the year 1991 when the Harshad Mehta scam happened. I have only explained by taking rice as an example, but the inflation rate of a country is determined by taking into account all major products and their increase in price over a period of time.

To know more about inflation read it here.

Why investing in FD is a bad idea?

Now you know what inflation is, so let’s see why it is a bad idea to invest in FD.

We all know what fixed deposit(FD) / recurring deposits(RD) is and at the max, you can get a return of 6.5%*.

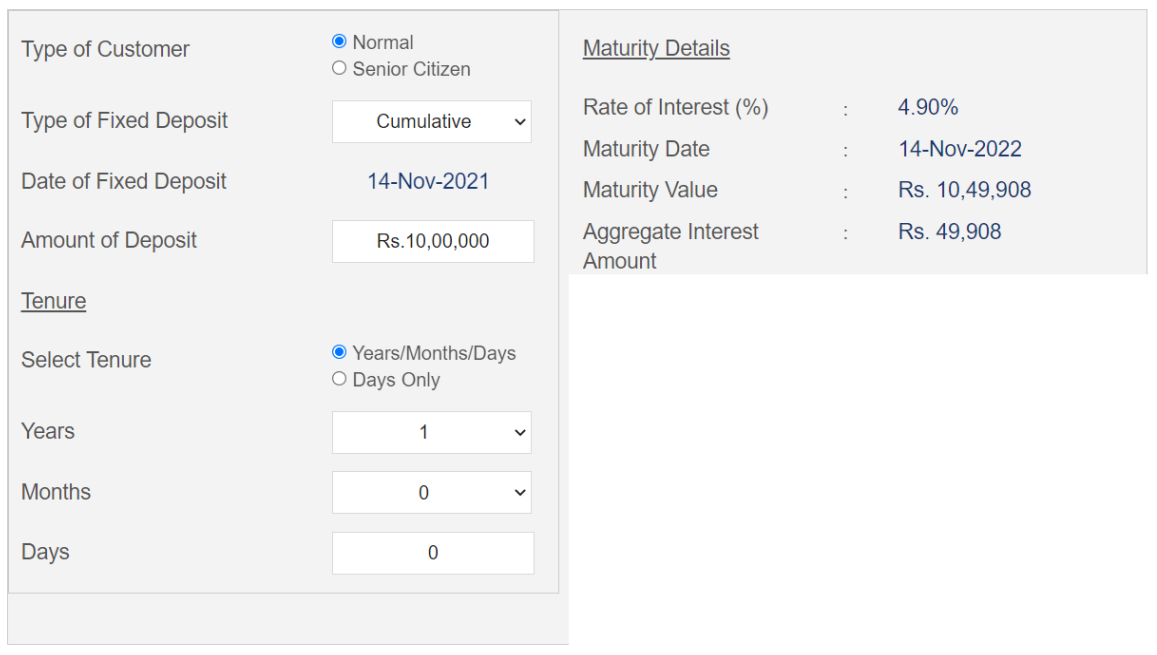

For example, you are opening an FD in an ICICI bank for 10 Lakh. You will get ~50k after 1 year with a rate of interest of 4.90% as shown below.

Most of us feel that 50k is a good return as banks provide only 3%*. We think that if our money stays idle in the bank it will generate only ~3%* return so let’s put it in FD and grow it at ~5%. This is where we all fail to consider the inflation rate.

For the above ICICI FD, we are getting a return of 4.90% and the inflation rate of 2021 is 5.56%. You haven’t gained anything instead you have lost your money by 0.66%.

Imagine, you have gained 5% in FD but the price of the commodities you want to buy also increased by 5% due to inflation then you haven’t gained in the actual sense. Ideally, your rate of return must beat the overall inflation rate, then only you have actually gained something in your hands.

I hope you get the idea why it is a bad idea to invest in FD. But FD can be an option for allocating your emergency funds.

If you put your money in equity you will get a rate of return of 10 - 15%* depending on the mutual fund and time period you are investing. I have written in detail about how your money will grow at a rate of 12% in this article. So if you get 12% you are beating the inflation by 6% and 6% is a huge return during a longer period.

Risks in Equity

Now we know that investing in FD is not so good idea, so shall we put all our money in equity?. The answer is NO!. We should never put all our money in Equity.

First of all, you should assess your risk profile because the equity market is subject to fluctuations and it can even wipe out your life savings if you don’t know why and where you are investing. Instead, if you are financially educated well you should be able to invest properly, monitor, and grow it.

If you are going to invest in equity then you should always have a long-term mindset. It is not recommended to invest in equity if you have a short-term goal of less than 5 years.

The usual formula for allocating your money in equity is 100 - (your age). For example, if your age is 25, you can allocate 75% of your money into equity instruments. This is not a definite formula, if your spouse is also earning well then you can allocate 90% of your money into equity based on your risk-taking capacity. It all depends from person to person.

😂Equity is subject to market risks. Please read all the documents carefully before you start making your investments😂. It’s true though, don’t take this statement as a joke.

*Rate of return is not fixed always. For FD it varies from bank to bank and for equity, it depends on the market performance.

To read about my previous articles on personal finance, click the Archive button and subscribe to my newsletter for weekly posts, and share it with your friends if you find it useful.

Did you learn something useful?

Follow us on Instagram - https://www.instagram.com/techmovfin/

Follow us on Twitter - https://twitter.com/techmovfin

Follow us on Facebook - https://www.facebook.com/techmovfin