EPF & PPF - Twists & Turns

EPF & PPF - Twists & Turns

A must know for everyone

Today, after a long break I want to write because this is such a compelling topic that I want everyone to be aware of. Read till the end to know about a piece of bonus information. Let’s go!!

What is EPF & PPF?.

As most of you might be knowing already, EPF is Employee Provident Fund, and PPF is Public Provident Fund. In general, EPF is called PF.

Both of these funds are aimed at providing you with financial freedom when you retire or at least you will have something in your hand at the time of retirement.

Are EPF & PPF the same?

The answer is NO!!. Though both are aimed towards retirement savings, there are some clauses that you need to know in-depth which we will be discussing further so that you can make an informed decision about where to invest and which is suitable for you.

Who can invest in EPF & PPF

In short, people who are employed and working for a recognized organization with 20 or more employees are eligible for investing in EPF and it will be taken care by your employer. EPF is managed by the Employees’ Provident Fund Organisation (EPFO) as per the Employees’ Provident Fund and Miscellaneous Act, 1952.

Anyone can open a PPF account irrespective of their job. Generally, people who are not working for recognized organizations or people who own businesses can invest in PPF for their retirement planning. PPF is also managed by EPFO.

Current Interest rate on EPF and PPF (As of FY - 2022)

The below interest rates are decided by the government and subject to change at any time by the government.

EPF - 8.5% p.a

PPF - 7.1% p.a

Lock-in Period & Withdrawal of funds

EPF is locked till retirement age i.e 58 years but you can withdraw on special occasions such as medical emergencies, marriage, or home loan repayment. To read more about EPF withdrawal process, click here . EPF can also be withdrawn while switching jobs from one company to another or two months after complete unemployment. Please be aware that you need to be complete 5 years of service in order to be exempt from taxes on returns during withdrawal.

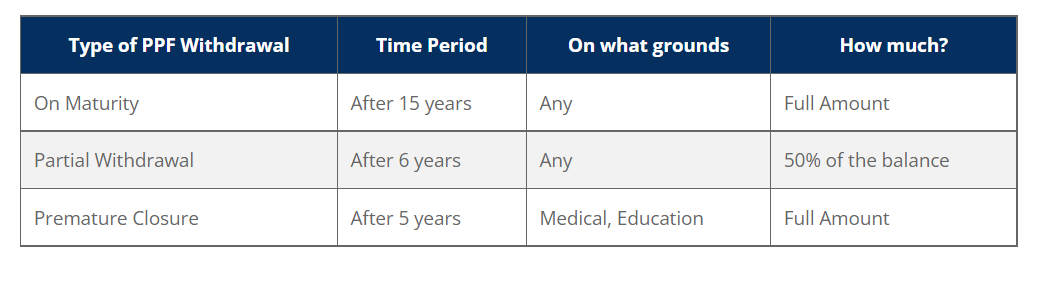

PPF lock in period is 15 years and it can be withdrawn completely after the completion of 15 years. Partial withdrawal after 6 years is possible and that too only 50% of the amount at the end of 4th year can be withdrawn & premature closure is also possible as shown below. To read more about PPF withdrawal click here

After 15 years of investment in PPF, an extension should be made for every 5 years to continue the PPF.

Taxation & Investment Limits

EPF contributions above 2.5 lakhs will be taxable. If you invest more than 2.5 lakhs, the interest earned on that excess amount will be considered for taxation.

PPF is fully tax-exempt and the investment limit is 1.5 lakhs in a financial year. Here the principal amount along with interest is non-taxable.

Where does EPF & PPF invest all our money?

According to the EPF rules, 12 percent of your salary must go towards your provident fund. Your company is also required to contribute the same 12 percent, out of which 8.33 percent of the salary is directed towards the Employee Pension Scheme or EPS. The remaining 3.67 percent are put into your EPF. - Source

The money pooled from all the employees are invested by a trust managed by the government and they invest on Exchange Traded Funds (ETFs) based on Nifty 50, Sensex, Central Public Sector Enterprises (CPSEs) & Bharat 22 Indices.Source

The amount invested in PPF is managed by the government(EPFO) and the EPFO decides what to do with the amount mostly government securities or bonds. In 2020 95% of the PPF funds went to FCI(Food Corporation of India) - Source

Currently, EPFO invests 15% of PPF funds in equity and this can change in future as discussions are going on - Source

BONUS - VPF

VPF is Voluntary Provident Fund where you can contribute more to the EPF account voluntarily by asking your HR to increase the EPF amount deducted. Why VPF is useful? EPF gives 8.5% return and is tax-free till 2.5 lakhs, so VPF is a good option for safe returns and it can be shown in 80C also. The lock-in period for VPF is 5 years and the rate of return is same as EPF.

A word of caution would be government is planning to increase the PF contribution so it will be wise to keep a watch on the PF changes which can come any time in the future. ELSS would be an alternate option but it has its own risks & rewards. So ultimately it boils down to your risk profile and asset allocation. I will cover ELSS in my upcoming posts if possible.

Thanks for reading till the end and if you liked it, share it with your friends. See you soon!!!